Japan’s Technology Paradox: World-Class Engineering, Weak Economic Growth

Original Article By SemiVision Research [Reading time: 19 mins]

Japan’s Technology Paradox: World-Class Engineering, Weak Economic Growth

At first glance, this chart looks like a simple ranking of the world’s ten largest economies.

But the real story is not the ranking.

The real story is the structural divergence behind the numbers.

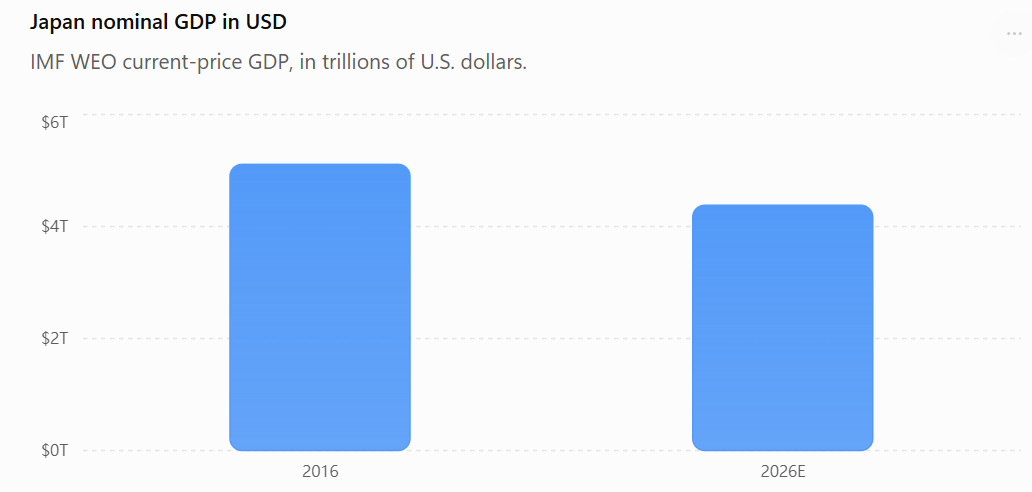

From 2016 to 2026, almost every major economy in the global top ten expanded in nominal U.S. dollar terms. The United States grew from roughly US$18.8 trillion to US$32.4 trillion. China expanded from US$11.5 trillion to US$20.9 trillion. India rose from US$2.3 trillion to US$4.2 trillion. Germany, the United Kingdom, France, and Italy also recorded meaningful growth.

Japan was the exception.

According to IMF nominal GDP figures in U.S. dollars, Japan’s economy declined from about US$5.1 trillion in 2016 to an estimated US$4.4 trillion in 2026, representing a roughly 14% decline over ten years.

This is not just a one-year fluctuation.

It is a signal.

The strange part is that Japan is not a country without technology. It is not a country without world-class companies. It is not a country without industrial capability.

Quite the opposite.

Japan remains one of the most irreplaceable countries in global semiconductors, materials, precision equipment, automotive technology, robotics, passive components, and high-end manufacturing.

So the key question is not:

Does Japan still have technological capability?

The answer is clearly yes.

The real question is much sharper:

Why has a country with world-class technology failed to convert that technological strength into macroeconomic growth?

The answer is not a single factor.

It is a full value-conversion problem.

Japan can push materials to the limit.

Japan can manufacture equipment that fabs cannot easily replace.

Japan can produce automobiles, components, and machines with world-class reliability.

Japan can drive quality, yield, and process control to extremely high levels.

But from technology to industry, from industry to platform, and from platform to capital formation, wage growth, domestic demand, and national GDP expansion, Japan’s conversion efficiency has lagged behind its engineering excellence.

That is the real warning behind Japan’s 14% GDP decline.

Do Not Misread the Number: Japan Did Not “Produce 14% Less”

The first point must be clarified.

This chart compares nominal GDP measured in U.S. dollars.

It is not real GDP.

It is not GDP measured in Japanese yen.

It is not purchasing-power-parity GDP.

It is not a direct measurement of physical output.

This distinction matters.

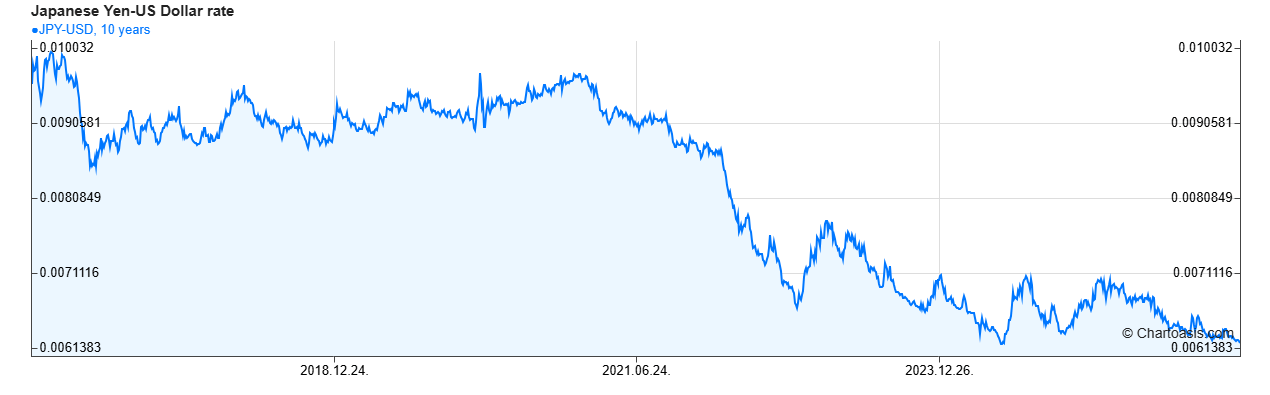

Japan’s GDP decline in U.S. dollar terms is heavily affected by currency depreciation. When the yen weakens against the dollar, Japan’s domestic economic output becomes smaller when translated into U.S. dollars, even if production, wages, and prices inside Japan do not fall by the same magnitude.

Therefore, saying that Japan’s GDP shrank by 14% does not mean that Japan’s real output collapsed by 14%.

That would be the wrong interpretation.

But it would also be wrong to dismiss the entire issue as “just exchange rates.”

Currency is not an isolated number.

Exchange rates reflect interest-rate differentials, inflation expectations, capital flows, long-term growth expectations, investment appetite, and a country’s relative position in global capital markets.

A weaker yen may be the direct mechanism that reduces Japan’s dollar GDP, but the currency movement itself reflects deeper economic realities.

When Japan’s GDP shrinks in U.S. dollar terms, it means Japan’s relative weight in the global economy becomes smaller.

Its global acquisition power declines.

Its ability to attract international talent becomes more difficult.

Its overseas investment capacity weakens in dollar terms.

Its companies face a different valuation environment.

Its national economic presence becomes less dominant relative to the United States, China, India, and other expanding economies.

In other words:

Currency is the amplifier. It is not the whole answer.

The deeper problem is structural.

Japan’s Biggest Structural Pressure Is Not China or the U.S. It Is Demographics.

The foundation of economic growth can be simplified into one equation:

GDP = Labor Force × Productivity × Capital Investment × Pricing Power

Japan’s biggest problem is the first variable: labor force.

Japan’s population is aging

Births continue to decline

The working-age population keeps shrinking.

The domestic market is becoming older and more mature.

This is no longer a future problem.

It is already a current operating constraint.

Restaurants lack workers.

Logistics companies lack drivers.

Construction companies lack labor.

Care facilities lack staff.

Retailers struggle with staffing.

Small and mid-sized manufacturers cannot find enough people.

When companies have demand but cannot find workers, demand cannot fully turn into output. When companies raise wages to attract labor but lack enough pricing power to pass those costs on to customers, margins are compressed. This is one of Japan’s core economic contradictions.

Japan does not lack skills. It does not lack process knowledge. It does not lack quality culture. But it lacks enough young workers to support long-term expansion. This labor constraint limits how much demand can be converted into production, service capacity, investment execution, and future growth.

Population decline also creates a second problem: weak incremental domestic demand. The United States can combine population growth, immigration, technology platforms, capital markets, and consumption expansion. India can combine young demographics, urbanization, digitalization, infrastructure demand, and manufacturing relocation. Japan faces a different reality: a mature market, an aging population, conservative consumption behavior, and limited domestic volume growth.

This means Japan is pressured from both sides. On the supply side, labor is constrained. On the demand side, domestic incremental growth is limited. That is why Japan’s demographic problem is not only a social issue. It is a macroeconomic ceiling.

Japan Became Too Good at Defense

After the collapse of Japan’s bubble economy, Japanese companies learned one critical lesson:

Survive.

Reduce debt.

Preserve cash.

Control costs.

Maintain employment stability.

Protect long-term supplier relationships.

Improve quality.

Avoid excessive risk.

This strategy made Japanese companies resilient.

It also created many hidden champions.

These companies may not dominate consumer headlines, but they dominate extremely important industrial niches. In materials, precision components, machine tools, semiconductor equipment, automotive parts, and factory automation, Japan still has a deep base of companies that global supply chains cannot easily replace.

But the global economy changed.

Over the past twenty years, the largest wealth creation did not only reward resilience.

It rewarded scale.

American technology companies built platforms.

Software, cloud infrastructure, developer ecosystems, data networks, and global user bases allowed them to replicate products across the world at very low marginal cost.

A platform company can add users, developers, applications, data, and monetization layers without rebuilding the entire physical supply chain each time.

That is why the capital market gives platform companies much higher valuation multiples.

Japan’s traditional model is different.

Japanese companies often create value by improving materials, equipment, components, and manufacturing processes. They make things more precise, more reliable, more durable, and more consistent.

This creates deep technical moats.

But it does not always create platform economics.

The contrast is simple:

Japan is excellent at making things better.

The United States is excellent at turning systems into platforms.

Both capabilities matter.

But in the past two decades, capital markets have rewarded platform control far more aggressively than incremental manufacturing excellence.

This is one reason Japan’s technology strength has not fully translated into GDP growth.

Its innovation often remains embedded inside the supply chain.

It creates value for the global system, but it does not always capture the largest share of the value pool.

What Japan Missed Was Not Just Software. It Was Value Capture.

It is easy to say Japan missed the software era.

But that statement is incomplete.

Japan did not simply miss software.

Japan missed a large part of the value-capture layer of the global digital economy.

The most valuable companies of the last two decades usually controlled four things:

Users.

Data.

Standards.

Ecosystems.

Apple controls devices, operating systems, services, and consumer loyalty.

Microsoft controls enterprise software, cloud infrastructure, developer workflows, and AI productivity tools.

Google controls search, advertising, Android, YouTube, and massive data infrastructure.

Amazon controls e-commerce, logistics, cloud infrastructure, and enterprise computing through AWS.

NVIDIA transformed GPUs into a full AI computing platform through CUDA, networking, systems, software libraries, and developer ecosystems.

These companies do not simply sell products.

They define rules.

They shape standards.

They capture usage.

They control platforms.

Japan has world-class companies: Sony, Toyota, Hitachi, Mitsubishi, Keyence, Tokyo Electron, Shin-Etsu, Murata, TDK, Nintendo, and many others.

But Japan does not have enough global digital infrastructure platforms.

That does not mean hardware is inferior to software.

The real issue is pricing power.

In modern technology markets, the company that controls the platform often captures the largest profit pool.

The suppliers may be technically essential, but the platform owner often determines architecture, pricing, ecosystem direction, and capital market narrative.

This creates Japan’s core contradiction:

Japan’s supply-chain position is very strong, but its value-distribution position is not strong enough.

Japan may supply the critical material.

Japan may provide the precision tool.

Japan may deliver the key component.

Japan may control the process know-how.

But the largest market capitalization may still accrue to the company controlling the platform, the brand, the cloud, the AI model, or the end customer.

This is why Japan can be indispensable and still underperform in GDP growth.

GDP Alone Underestimates Japan’s Strategic Value

If we look only at GDP, Japan appears to be a declining economy.

But if we look at the semiconductor supply chain, Japan remains extremely important.

In many parts of the semiconductor ecosystem, Japan is not peripheral.

Japan is foundational.

From silicon wafers, photoresists, specialty chemicals, and packaging materials to coating and developing systems, cleaning tools, deposition equipment, inspection, testing, dicing, grinding, and polishing, Japanese companies occupy critical nodes.

Tokyo Electron.

SCREEN.

Kokusai Electric.

Advantest.

Lasertec.

DISCO.

Shin-Etsu.

SUMCO.

TOK.

JSR.

Resonac.

Ajinomoto.

These are not just company names.

They are infrastructure.

Modern AI chips are not created by GPU design alone.

They require advanced process technology.

They require EUV-related materials and process control.

They require high-quality wafers.

They require photoresists and specialty chemicals.

They require precision cleaning and deposition.

They require HBM.

They require advanced packaging.

They require substrates, underfill, molding, bonding, dicing, grinding, and inspection.

They require high-end test equipment.

They require a deep base of manufacturing know-how.

Japan participates in many of these layers.

This is why Japan should not be misunderstood as a country that has lost industrial relevance. Japan is still one of the pillars of the global semiconductor system. Its strengths in materials, equipment, precision manufacturing, passive components, chemicals, substrates, process control, and reliability engineering remain deeply embedded in the global technology supply chain.

But this creates another question: if Japan is so important, why does that importance not show up more clearly in GDP growth? The answer is that strategic importance and macroeconomic expansion are not the same thing. A country can be indispensable in a specific part of the supply chain but still fail to generate broad-based national growth.

A small number of globally competitive companies can be extremely strong, while the broader domestic economy remains stagnant. Semiconductor equipment and materials can deliver high margins, but their market size is still constrained by global fab capital expenditure cycles. Japanese companies can generate profits globally, but not all production, investment, wages, and innovation spillovers necessarily remain inside Japan.

Technology strength inside one layer of the value chain does not automatically become a national growth engine. It must be scaled. It must be integrated. It must be converted into platforms, ecosystems, clusters, talent flows, capital formation, and domestic productivity gains. This is where Japan still has work to do.

Japan Is a Supply-Chain Power, But Not the Center of Demand

Japan remains highly relevant in the AI era because it provides many of the tools and materials that allow others to produce AI hardware.

But high GDP growth usually comes from three forces.

First, a large and expanding domestic market.

Second, globally scalable high-margin products or platforms.

Third, capital markets that reward growth with high valuations, enabling investment, hiring, acquisitions, and new company formation.

Japan has part of the second force.

It has excellent high-margin industrial products.

But it is weaker in the first and third forces.

Its domestic market is mature and aging.

Its capital market has improved, but it still does not create the same scale of technology wealth formation as the United States.

Its startup ecosystem is growing, but it remains smaller and less aggressive than Silicon Valley, China’s technology ecosystem, or India’s digital economy.

Japan can supply the world’s best materials and machines, but the biggest value capturers in the AI era are still concentrated elsewhere.

The United States controls many of the leading AI platforms, GPUs, cloud companies, software layers, and capital markets.

Taiwan controls a critical part of advanced semiconductor manufacturing and packaging.

South Korea controls key memory technologies, especially HBM and DRAM.

China is building enormous industrial scale and domestic demand.

India is building a large digital economy with demographic momentum.

Japan is powerful, but its power is often upstream, specialized, and supply-chain based.

That is strategically important.

But it is not the same as being the center of end demand.

This is Japan’s challenge in the AI era:

Japan is located at the foundation of the AI hardware stack, but it has not yet returned to the top of the value-capture stack.

India’s Rise Shows What Japan Lacks: Incremental Growth

The same GDP chart also highlights India’s rise. From 2016 to 2026, India’s nominal GDP in U.S. dollars increased from roughly US$2.3 trillion to US$4.2 trillion, representing more than 80% growth. This does not mean India’s technology base has surpassed Japan’s across all industries. It means India has what Japan lacks: incremental growth.

India has a young population, while Japan has an aging population. India is still urbanizing, while Japan is already highly urbanized. India has massive unmet demand in housing, transportation, digital services, infrastructure, finance, healthcare, and consumption, while Japan is already a mature consumer market. India can still grow by formalizing, digitizing, building, connecting, and upgrading. Japan, by contrast, must grow mainly through productivity gains, automation, export competitiveness, and value capture. That is a much harder path.

Japan’s advantage is maturity. Maturity brings reliability, institutional depth, quality, safety, engineering discipline, supply-chain trust, and high income levels. But maturity also limits growth. India’s advantage is that it is not yet mature. Immaturity creates inefficiency, but it also creates room for expansion.

For global investors, that difference matters. When capital seeks stability, Japan is attractive. When capital seeks growth, capital flows to India, U.S. technology platforms, and other emerging markets. This is why Japan can remain wealthy, advanced, and strategically indispensable while still facing pressure in GDP rankings. Japan is not disappearing, but its relative share of global growth is declining.

The AI Era Gives Japan a Chance to Be Repriced

Japan’s future is not hopeless.

In fact, the AI era may increase Japan’s strategic importance.

The reason is simple:

AI is not only software.

AI needs chips.

AI needs data centers.

AI needs power systems.

AI needs thermal management.

AI needs advanced packaging.

AI needs HBM.

AI needs substrates.

AI needs high-end materials.

AI needs precision equipment.

AI needs robotics.

AI needs sensors.

AI needs motors.

AI needs factory automation.

AI needs high-reliability components.

These are exactly the areas where Japan has decades of accumulated strength. Japan does not need to copy the United States and build another Google. It may not need to create another NVIDIA. Japan’s opportunity is different: it can become one of the most important industrial foundations of the AI hardware era.

Semiconductor manufacturing needs Japanese tools and materials. Advanced packaging needs precision equipment, bonding, dicing, grinding, cleaning, substrates, films, chemicals, and inspection. Data centers need high-reliability components, power electronics, thermal materials, passive components, and precision manufacturing. Robotics and automation need motors, sensors, controllers, machine tools, mechanical engineering, and system integration. These are not abstract advantages. They are areas where Japan already has deep industrial capability, long-term process knowledge, and globally trusted suppliers.

Aging societies also need labor-saving technologies. This is where Japan can turn a disadvantage into an advantage. Japan’s demographic crisis can become a forcing function for automation. When labor shortages affect healthcare, logistics, manufacturing, retail, and services, automation is no longer optional. It becomes national infrastructure.

If Japan can use its own aging society as a real-world testbed for AI robotics, smart factories, autonomous logistics, and elderly-care automation, it may develop exportable systems for other aging economies. Europe will age. South Korea will age. China will age. Taiwan will age. Even parts of the United States will face labor shortages in key sectors. If Japan can build scalable solutions first, its demographic weakness could become an industrial first-mover advantage.

TSMC Kumamoto Is More Than a Fab

TSMC’s Kumamoto fab is an important symbol. It is not only about semiconductor capacity; it is about Japan reconnecting with the global advanced manufacturing network. For Japan, the question is not simply whether subsidies can attract one fab. The deeper question is whether one fab can become a cluster.

A fab is capacity. A cluster is growth. Capacity means wafers. A cluster means engineers, suppliers, materials, equipment, universities, startups, logistics, process knowledge, customer relationships, and long-term regional investment. If Japan can use semiconductor investment to rebuild industrial clusters, the impact can go far beyond chip production.

It can create new jobs, attract young engineers, bring overseas supply chains back into Japan, and connect Japanese materials and equipment companies more deeply with global foundry demand. It can also create new opportunities for startups, advanced manufacturing services, testing, automation, logistics, and regional industrial development.

This is why semiconductor policy matters. Semiconductors are no longer just one industry. They are a national industrial platform connecting energy, defense, AI, automotive, robotics, cloud computing, telecommunications, and advanced manufacturing. Japan understands this. The question is whether Japan can execute quickly enough.

The Core Problem: Japan Converts Technology Into Products, But Not Enough Into Platforms

Japan’s engineering ability remains world-class. Few countries can match Japan’s depth in precision manufacturing, materials science, components, equipment, reliability engineering, and process discipline. But the next stage of competition requires something more difficult. Japan must convert technology into systems, systems into platforms, platforms into pricing power, and pricing power into capital formation, wage growth, talent attraction, and domestic reinvestment. This is the conversion chain Japan needs to repair.

A country cannot rely only on excellent components. Excellent components are necessary, but they are no longer sufficient. In the modern technology economy, the largest value often belongs to the party that controls the architecture. The company that controls the architecture defines the ecosystem. The company that defines the ecosystem captures recurring revenue. The company that captures recurring revenue receives a higher valuation. And the company with a higher valuation can hire better talent, acquire strategic assets, invest more aggressively, and shape the next generation of technology.

This is how platform economies compound. Technology alone does not automatically become economic power. Engineering strength must be translated into system-level leadership, business model control, ecosystem influence, and financial scalability. Without that conversion, even the most advanced components may become critical but undervalued pieces inside someone else’s architecture.

Japan’s challenge is therefore not whether it still has technology. It does. The real challenge is whether Japan can move from component excellence to system leadership, from system leadership to platform control, and from platform control to value capture. That is the difference between being essential and being dominant.

Japan is still essential. But can Japan become dominant again? That is the real question.

Conclusion: Japan Did Not Lose in Technology. It Lost in Value-Conversion Efficiency.

Japan’s nominal GDP in U.S. dollars declined from roughly US$5.1 trillion in 2016 to an estimated US$4.4 trillion in 2026.

The decline reflects at least four overlapping forces.

First, yen depreciation reduced Japan’s GDP after conversion into U.S. dollars.

Second, aging demographics and a shrinking labor force weakened long-term growth on both the supply and demand sides.

Third, decades of low inflation, low risk appetite, and conservative corporate investment limited nominal economic expansion.

Fourth, Japan missed much of the platform economy’s most powerful growth cycle and did not fully capture the premium from software, ecosystems, global user networks, and capital markets.

But this does not mean Japan has no future.

Japan still controls critical capabilities in semiconductor equipment, materials, precision manufacturing, robotics, automotive components, passive components, and industrial automation.

As AI hardware demand grows, these capabilities will become more strategically valuable.

The real question is whether Japan can upgrade from:

Supply-chain indispensability to Value-distribution indispensability.

If Japan continues to serve mainly as the world’s most reliable supplier behind the technology industry, it will remain important.

But its GDP ranking may continue to decline.

If Japan can integrate semiconductors, AI hardware, robotics, automation, energy systems, and materials technology into exportable industrial platforms, it has a chance to become a growth engine again.

That is the true lesson of this GDP chart.

Japan does not lack technology.

But technology alone is not enough.

A country must turn technology into industry.

Industry into platforms.

Platforms into pricing power.

Pricing power into investment, wages, talent, and international influence.

Japan’s next decade will not be defined by whether it can still manufacture the world’s best components.

It will be defined by whether it can move from being a world-class supplier to becoming a world-class growth engine again.

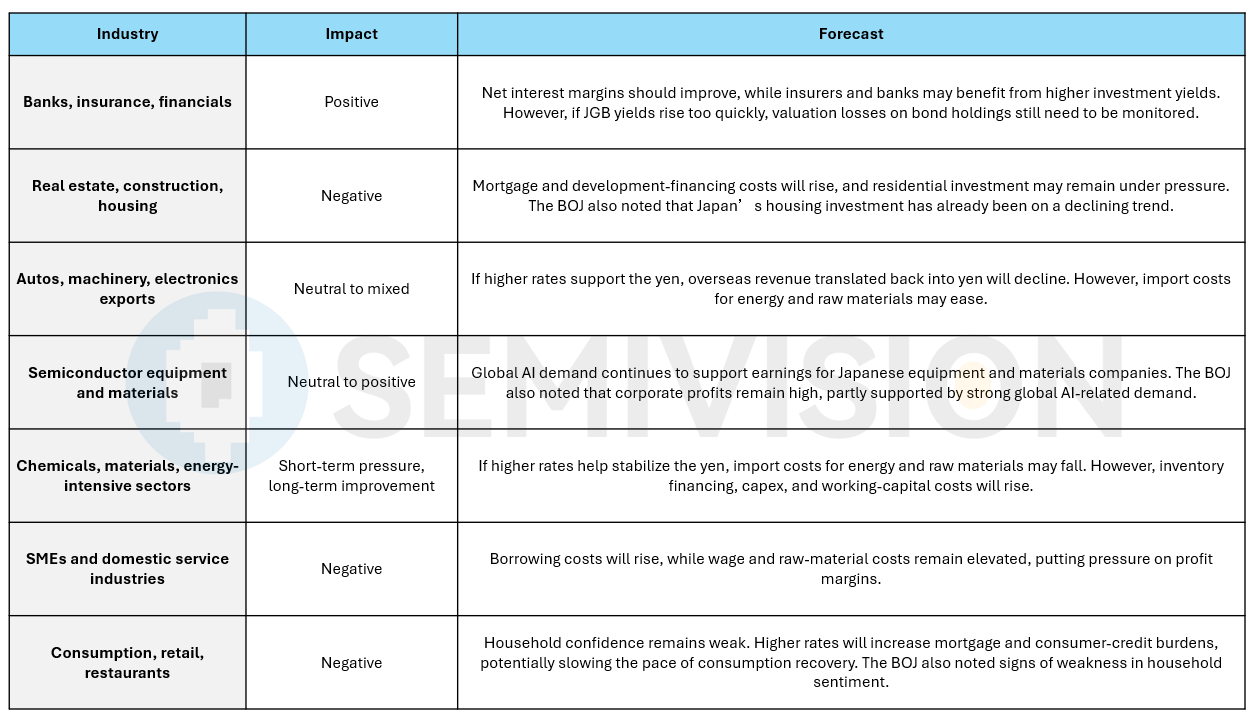

On June 16, 2026, the Bank of Japan announced that it would raise its short-term policy rate from 0.75% to around 1.0%, an increase of 25 basis points. The decision was approved by a 7–1 vote, and both Reuters and the Financial Times described this as Japan’s highest policy-rate level since 1995. The BOJ’s official statement also emphasized that even after the rate hike, Japan’s financial conditions remain accommodative, real interest rates remain negative, and corporate funding demand, as well as CP and corporate bond issuance conditions, remain relatively favorable.

A refined version would be:

At its monetary policy meeting on June 16, 2026, the Bank of Japan raised its short-term policy rate by 25 basis points, from 0.75% to around 1.0%, bringing Japan’s policy rate to its highest level since 1995. This marks the later stage of Japan’s exit from the ultra-low interest-rate era. The BOJ’s core concern is not simply to suppress demand, but to prevent energy prices, food prices, wage growth, and corporate price pass-through from developing into a broader inflation cycle.

For Japanese industries, the short-term impact is higher cost pressure, while the medium-term implication is a reassessment of capital allocation.

SemiVision view: this rate hike will not immediately derail Japan’s industrial recovery, but it will accelerate industrial differentiation.

First, the financial sector will benefit from the normalization of interest rates. Japanese banks have been constrained by zero and near-zero interest rates for decades. With the policy rate now at 1%, banks have room to improve net interest margins, while insurers can allocate long-term assets at higher yields.

Second, highly leveraged, low-margin, domestically oriented industries will come under pressure. Real estate, construction, retail, restaurants, and SMEs will be the first to feel the impact of higher funding costs. Japanese companies have long been accustomed to cheap capital. As interest rates normalize, firms without pricing power or productivity gains will be forced to restructure.

Third, for export-oriented manufacturers, the key variable is the yen, not the interest rate itself. If the rate hike causes the yen to appreciate significantly, companies such as Toyota, Sony, Keyence, Murata, TDK, Tokyo Electron, and SCREEN may face pressure from weaker yen-translated overseas earnings. But if the yen merely stabilizes rather than strengthens sharply, the impact could be positive by lowering import costs for energy, chemicals, metals, and equipment.

Fourth, Japan’s semiconductor equipment and materials industries will not lose competitiveness simply because rates rise to 1%. Japan’s advantages in semiconductor materials, manufacturing equipment, passive components, power semiconductors, and precision processing equipment come from technology barriers, customer qualifications, and global AI capex—not from low interest rates. The real question is whether Japanese companies will use their cash to invest in AI, semiconductors, batteries, robotics, and advanced materials, rather than continuing to hold cash conservatively.

Therefore, the BOJ’s rate hike to 1% is not merely a monetary-policy event. It is a signal of a structural turning point for Japanese industry. As the era of cheap capital comes to an end, Japanese companies will gradually shift from relying on a weak yen and low interest rates to generating value through technology, efficiency, pricing power, and their strategic position in the global supply chain. For Japan, this is both a source of pressure and the beginning of a new process of industrial competitiveness screening.