Taiwan’s Next Semiconductor Bottleneck Is Not Silicon. It Is Power.

Original Article By SemiVision Research [Reading time: 10 mins]

ECOC, the European Conference on Optical Communications, is the largest and most prestigious event on optical communications in Europe and the second largest worldwide. At ECOC, researchers from both industry and academia and professionals come together to discuss and explore advances and probe future trends that will enable scientific progress and economic growth.

The ECOC Exhibition runs in parallel with the ECOC conference and has become the largest optical communications exhibition in Europe and the key meeting place for decision-makers in the optical communications world.

Join us in Málaga, where we expect to reach a record number of attendees, and enjoy the charming and vibrant scientific and business atmosphere of this historic Mediterranean city.

https://www.ecoc2026.org/ECOC2026

Taiwan’s Next Semiconductor Bottleneck Is Not Silicon. It Is Power.

For the past decade, the world has described Taiwan through one dominant lens: semiconductors.

Taiwan makes the chips.

Taiwan packages the chips.

Taiwan enables AI servers, smartphones, cloud infrastructure, automotive electronics, and increasingly, national security systems.

But as AI computing moves from model training to large-scale deployment, a more fundamental question is emerging:

Can Taiwan supply enough power, at the right location, with enough resilience, and with enough low-carbon credibility to support the next phase of global semiconductor growth?

That is the central message behind Taipower Chairman Tseng Wen-sheng’s presentation, Resilience Blueprint: Power Resilience and International Competitiveness. The presentation’s key sentence is simple but strategically important: “Electricity is competitiveness.”

In the AI era, power is no longer a utility issue. It is an industrial strategy issue. It is a semiconductor supply chain issue. It is a geopolitical issue.

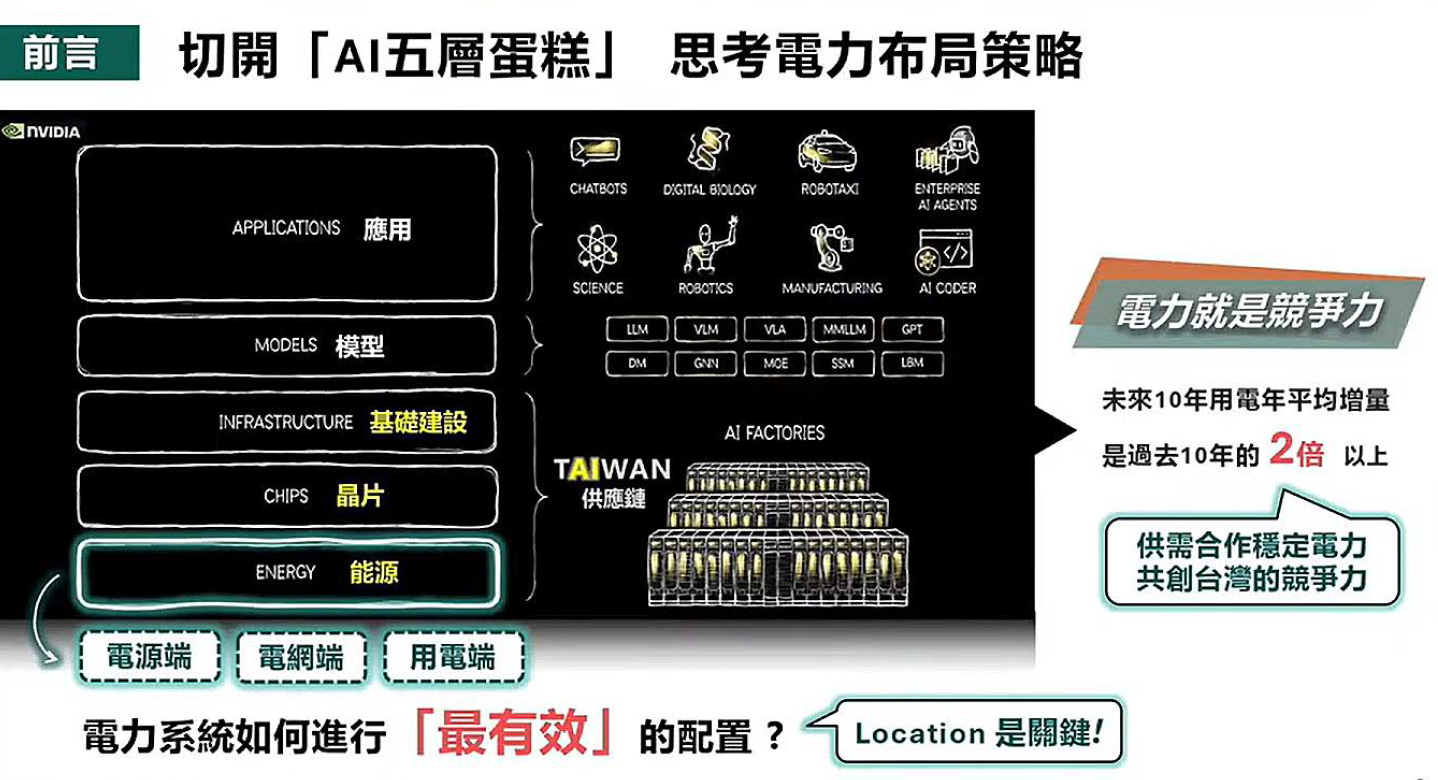

The AI Stack Has a Hidden Bottom Layer: Energy

The global AI industry usually talks about applications, models, infrastructure, and chips.

Applications are what users see: chatbots, robotics, digital biology, AI agents, manufacturing automation, and AI coding.

Models are the software intelligence layer: LLMs, VLMs, MoE models, diffusion models, world models, and other architectures.

Infrastructure is the cloud and data center layer.

Chips are the visible hardware layer: GPUs, ASICs, CPUs, networking chips, HBM, advanced substrates, CoWoS, SoIC, and optical interconnects.

But beneath all of them is a layer that is easier to ignore and harder to replace:

Energy.

Without electricity, there is no AI factory.

Without grid capacity, there is no data center cluster.

Without stable power, there is no advanced fab.

Without low-carbon power, there is no credible global manufacturing footprint.

This is why the presentation uses the concept of the “AI five-layer cake” to rethink power deployment strategy. Energy is not outside the AI stack. Energy is the foundation of the AI stack.

The implication is direct: Taiwan’s semiconductor competitiveness will increasingly depend not only on process technology, packaging capacity, and talent, but also on whether the power system can scale with AI-era demand.

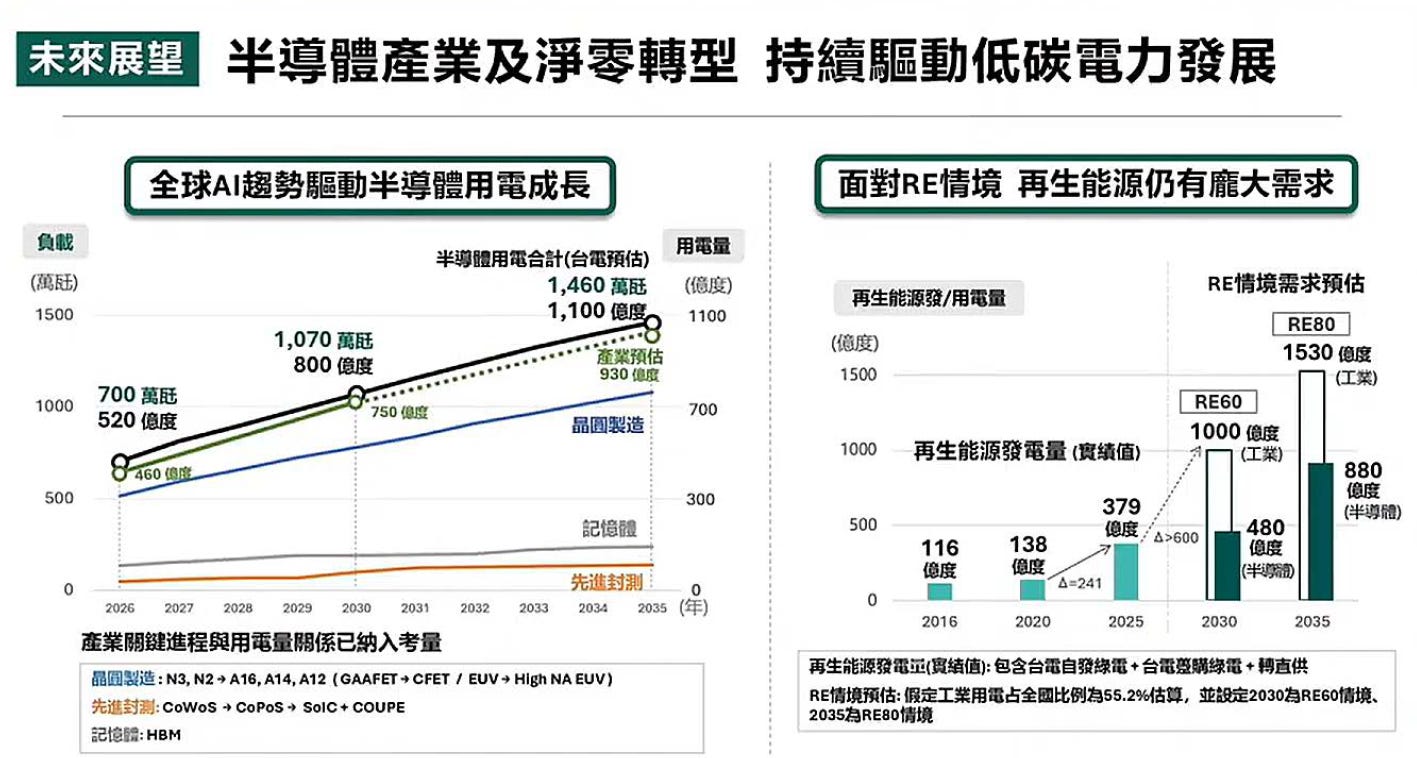

The Semiconductor Industry Is Becoming a Power-Dense Industry

Semiconductor manufacturing has always required stable electricity. But advanced semiconductor manufacturing is entering a new power-density regime.

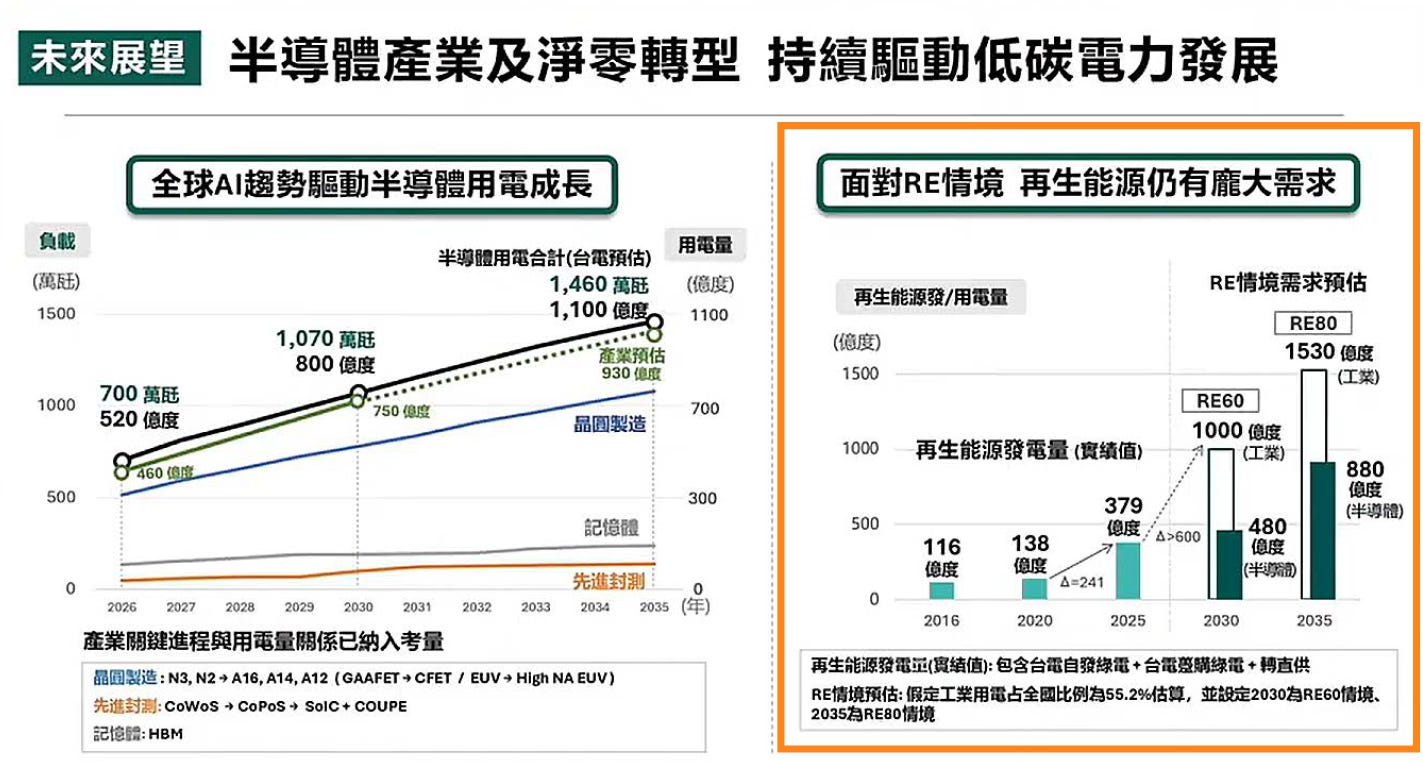

The Taipower presentation estimates that semiconductor-related electricity demand will rise sharply from 2026 to 2035. According to the slide, semiconductor electricity demand is projected to move from roughly 52 billion kWh in 2026, to 80 billion kWh in 2030, and potentially 110 billion kWh by 2035. Peak power demand is also projected to rise from about 7 GW in 2026, to 10.7 GW in 2030, and 14.6 GW by 2035.

This demand is not random. It is structurally linked to three semiconductor transitions.

First, wafer manufacturing is moving from N3 and N2 toward A16, A14, A12, GAAFET, CFET, EUV, and High-NA EUV.

Second, advanced packaging is moving from CoWoS toward CoPoS, SoIC, and more complex system-level integration.

Third, memory is being pulled by HBM and AI server demand.

Each transition improves computing capability. But each transition also increases fab complexity, process steps, cleanroom intensity, tool density, thermal load, test time, and infrastructure burden.

In other words, semiconductor scaling is no longer only about transistor density. It is also about electricity density.

AI Data Centers Change the Geography of Power

Traditional electricity planning often focused on cities, residential areas, industrial parks, commercial districts, and science parks.

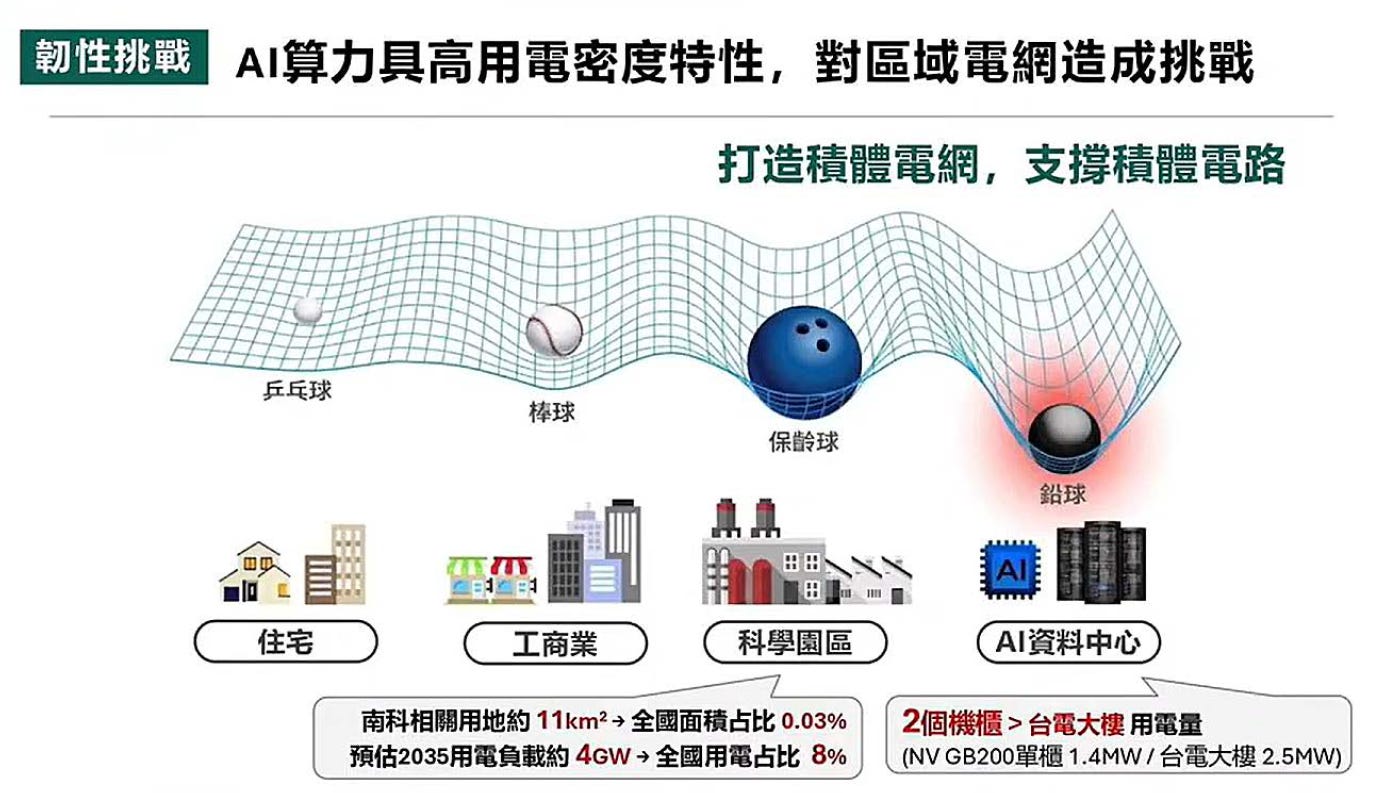

AI data centers introduce a new type of load: highly concentrated, highly power-dense, and highly location-sensitive.

The presentation uses a powerful analogy: different types of electricity users are like different balls placed on a grid surface. Residential demand may be like a ping-pong ball. Commercial demand may be like a baseball. Science parks may be like a bowling ball. But AI data centers are closer to a lead ball.

The problem is not just total electricity consumption. The problem is local grid stress.

A national grid may have enough theoretical electricity supply, but if the demand is concentrated in one location faster than transmission and distribution infrastructure can be built, the local grid becomes the bottleneck.

This matters deeply for Taiwan. The presentation points out that the Southern Taiwan Science Park occupies only around 11 square kilometers, about 0.03% of Taiwan’s total land area, but its estimated load could reach around 4 GW by 2035, representing about 8% of national electricity consumption.

That is the new AI-era contradiction:

The most valuable industrial output may come from an extremely small geographic area, but the power requirement behind that output is national in scale.

This is why location becomes strategy. The question is no longer simply “Where can we build the fab or data center?” The better question is:

Where can power, land, transmission, renewable energy, water, labor, logistics, and industrial customers be matched most efficiently?

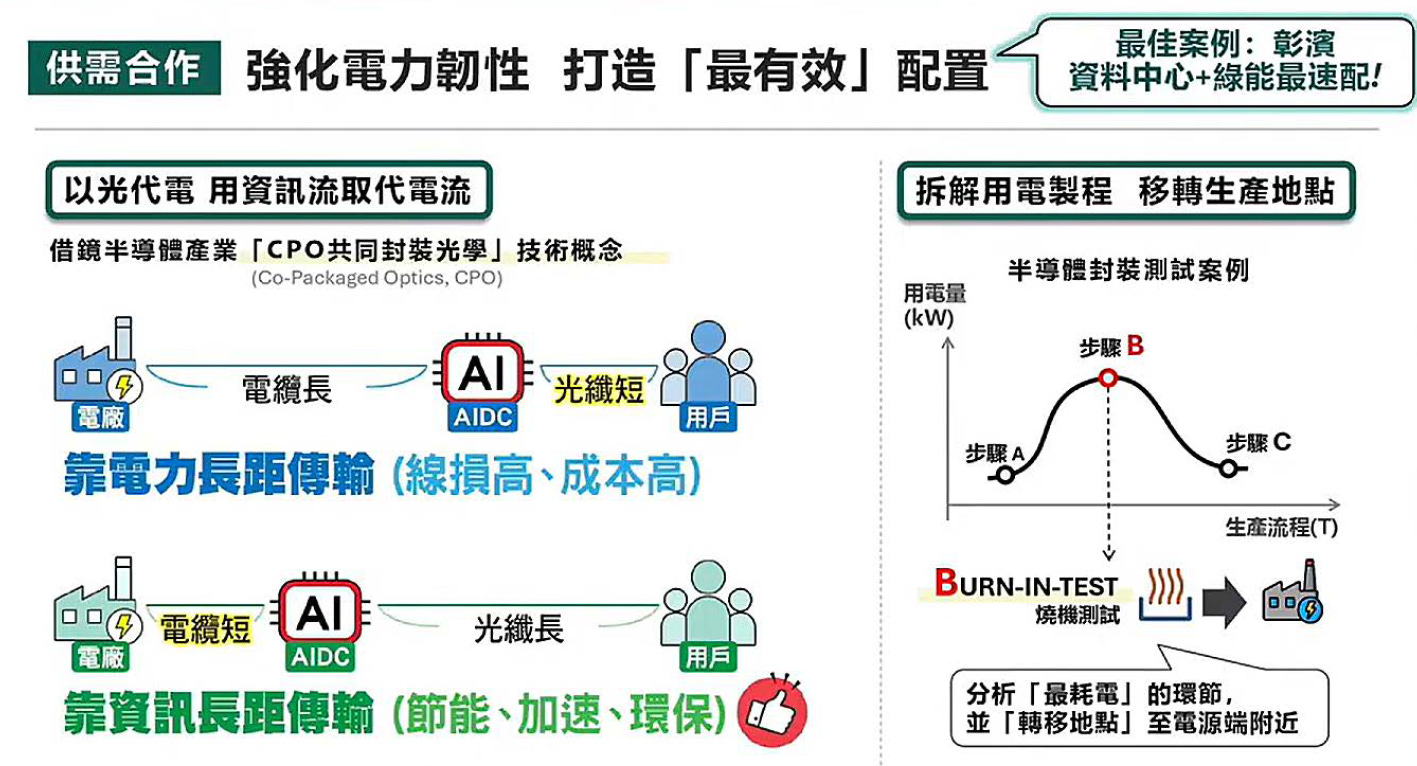

The New Rule: Move Data, Not Electricity

One of the most important ideas in the presentation is the shift from long-distance power transmission to long-distance information transmission.

The slide compares two models.

In the first model, the power plant is far away from the AI data center, while users are nearby. Electricity has to travel over long distances. This creates higher line losses and higher grid infrastructure costs.

In the second model, the AI data center is placed closer to the power source. Electricity transmission distance becomes shorter, while optical fiber carries data over longer distances. This is more efficient because information can travel through fiber with far lower loss than bulk electricity transmission through long power lines.

The presentation connects this logic to the semiconductor industry’s CPO concept. In chip packaging, co-packaged optics tries to shorten electrical paths and use optical links for high-speed data transmission. At the power infrastructure level, the same principle can apply:

Shorten the electricity path. Lengthen the optical path.

This has major implications for Taiwan’s AI infrastructure policy.

Instead of putting every AI data center near existing industrial or urban centers, Taiwan may need to think about power-first locations. Data centers could be placed closer to renewable energy zones, power plants, substations, or grid-ready industrial areas. Users do not need to be physically close to the AI server. They need low-latency connectivity, reliable service, and scalable compute.

In the AI era, optical fiber may become a form of energy strategy.

Advanced Packaging and Burn-In May Become Relocatable Loads

Another important concept in the presentation is the decomposition of semiconductor electricity demand.

Not every process step has the same location requirement.

Some steps must be close to fabs, suppliers, engineers, and cleanroom ecosystems. But some steps are more electricity-intensive than location-sensitive.

The presentation gives semiconductor packaging and testing as an example, especially burn-in testing.

Burn-in is energy-intensive because devices are stressed under elevated temperature and operating conditions to screen reliability issues. In the presentation’s framework, if a process step has high electricity consumption but relatively more flexible location requirements, it may be possible to move that step closer to the power source.

This is a very important industrial policy idea.

In the past, semiconductor clusters were built mainly around process integration, talent, customers, and supply chain density. In the future, electricity availability may become another sorting mechanism.

High-value, process-sensitive steps may remain in dense semiconductor clusters.

High-power, location-flexible steps may migrate toward power-advantaged regions.

AI data centers may be planned around grid nodes and renewable supply.

Packaging, testing, and burn-in may become part of demand-side power optimization.

This means Taiwan’s semiconductor map could gradually evolve from a pure manufacturing cluster map into a power-aware manufacturing network.

Renewable Energy Demand Will Keep Rising

Power resilience is not only about quantity. It is also about carbon quality.

Global semiconductor customers increasingly care about renewable energy procurement. This is not only ESG branding. It is part of supply chain qualification, carbon accounting, customer contracts, and international competitiveness.

The presentation estimates strong renewable energy demand under RE60 and RE80 scenarios. Under the RE60 scenario for 2030, industrial renewable demand could reach around 100 billion kWh, with semiconductor demand around 48 billion kWh. Under the RE80 scenario for 2035, industrial renewable demand could reach around 153 billion kWh, with semiconductor demand around 88 billion kWh.

The message is clear: renewable energy is still structurally undersupplied relative to future semiconductor and AI demand.

For Taiwan, this creates a dual challenge.

The country must increase total power supply, but it must also increase low-carbon power availability. It must serve rising AI and semiconductor loads, but it must also meet international customer expectations. It must maintain reliability while expanding renewable penetration. It must add generation, storage, grid flexibility, and transmission infrastructure at the same time.

This is not easy. But it is unavoidable.

The next semiconductor competition will not only ask: who has the best process node?

It will also ask: who has the cleanest, most resilient, and most scalable power system?

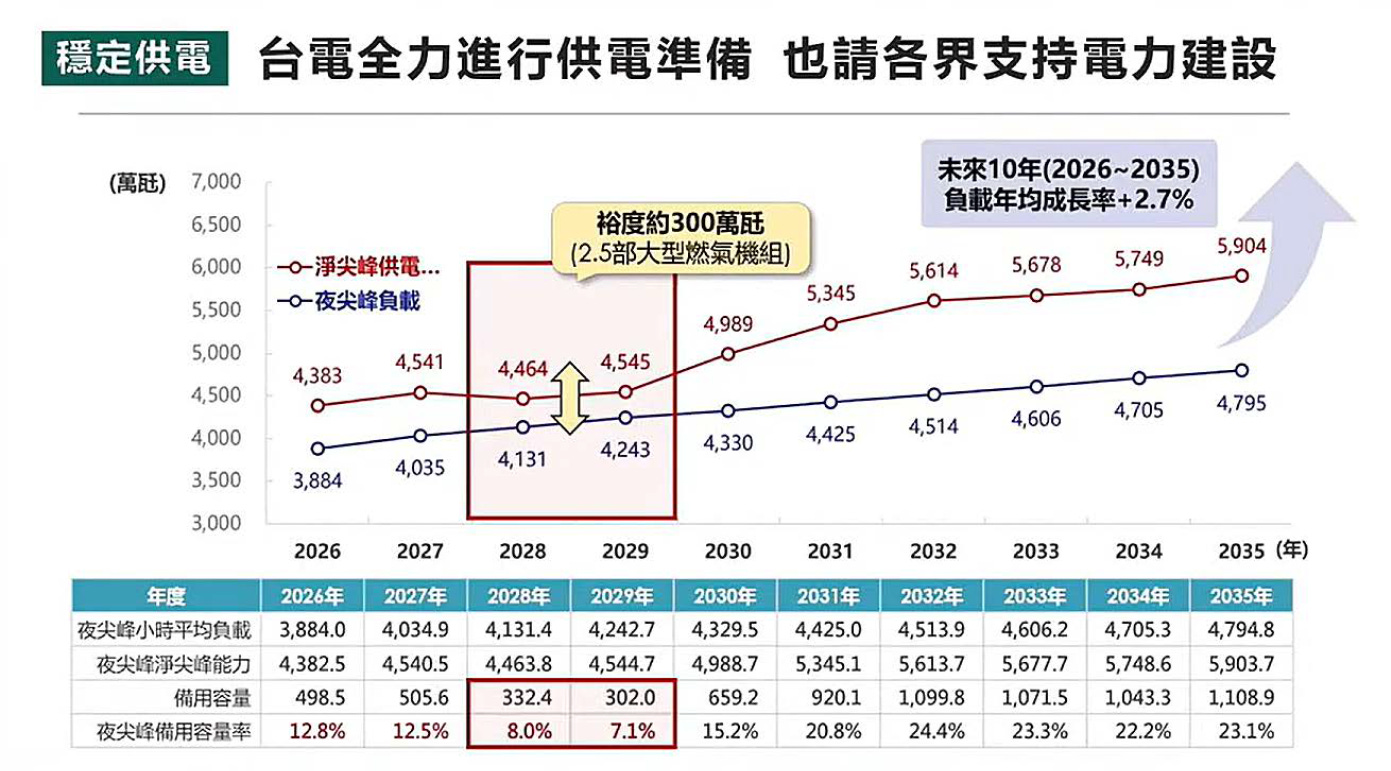

The 2028–2029 Window Looks Critical

The presentation’s final slide shows Taiwan’s supply preparation from 2026 to 2035. The long-term trend suggests annual load growth of about 2.7% over the decade.

But the most sensitive period appears to be 2028–2029.

The chart shows reserve margins declining to around 8.0% in 2028 and 7.1% in 2029, before recovering from 2030 onward. The slide also notes a margin of roughly 3 million kW, equivalent to about 2.5 large gas-fired power units.

This does not necessarily mean a crisis is guaranteed. But it does mean the transition window is tight.

For semiconductor investors and supply chain executives, this is the key point: Taiwan’s power strategy cannot be evaluated only by 2035 capacity targets. The execution risk lies in the middle years, when demand growth, generation projects, grid upgrades, renewable procurement, and industrial expansion schedules must all align.

The semiconductor industry is used to thinking in technology roadmaps: N2, A16, CoWoS, HBM4, glass substrate, CPO, 800V power architecture.

Taiwan now needs an equally disciplined power roadmap.

Electricity Is Becoming Part of Semiconductor Due Diligence

For global customers, Taiwan’s semiconductor value proposition has always been built on trust.

Trust in yield.

Trust in delivery.

Trust in engineering execution.

Trust in ecosystem density.

Trust in crisis response.

In the AI era, that trust must extend to electricity.

When customers evaluate semiconductor capacity, they will increasingly ask:

Can the fab get enough power?

Can the data center connect fast enough?

Can the science park scale without local grid congestion?

Can the supplier meet renewable energy commitments?

Can the region withstand typhoons, heat waves, grid stress, and geopolitical uncertainty?

Can the electricity infrastructure keep pace with AI demand?

This means power resilience will become part of semiconductor due diligence.

It will affect site selection, supplier qualification, customer allocation, long-term purchase agreements, and national industrial strategy.

For Taiwan, the opportunity is large. If Taiwan can solve the power problem, it can reinforce its role as the world’s most important AI hardware manufacturing base. If it cannot, electricity may become the next structural bottleneck after CoWoS capacity, HBM supply, substrate availability, and thermal management.

The Strategic Conclusion: No Power, No Compute

The AI industry likes to talk about compute.

But compute is not abstract. Compute is physical.

It requires silicon.

It requires packaging.

It requires memory.

It requires substrates.

It requires cooling.

It requires land.

It requires water.

It requires transmission lines.

It requires substations.

It requires renewable energy.

It requires political execution.

Taiwan has already proven that it can build the world’s most advanced semiconductor manufacturing ecosystem. The next challenge is to build the power architecture that allows that ecosystem to keep scaling.

The old semiconductor slogan was:

No chip, no AI.

The new industrial reality is:

No power, no compute. No grid, no AI factory. No resilience, no competitiveness.

Taiwan’s next semiconductor advantage may not come only from another process node or another packaging platform. It may come from the ability to integrate power planning, grid resilience, renewable energy, AI data centers, and semiconductor manufacturing into one national competitiveness blueprint.

In the age of AI, electricity is no longer just the cost of doing business.

Electricity is the business.