The AI Boom Has a Memory Problem — South Korea Is Spending KRW800 Trillion to Solve It

Original Article By SemiVision Research [Reading time: 10 mins]

The AI Boom Has a Memory Problem — South Korea Is Spending KRW800 Trillion to Solve It

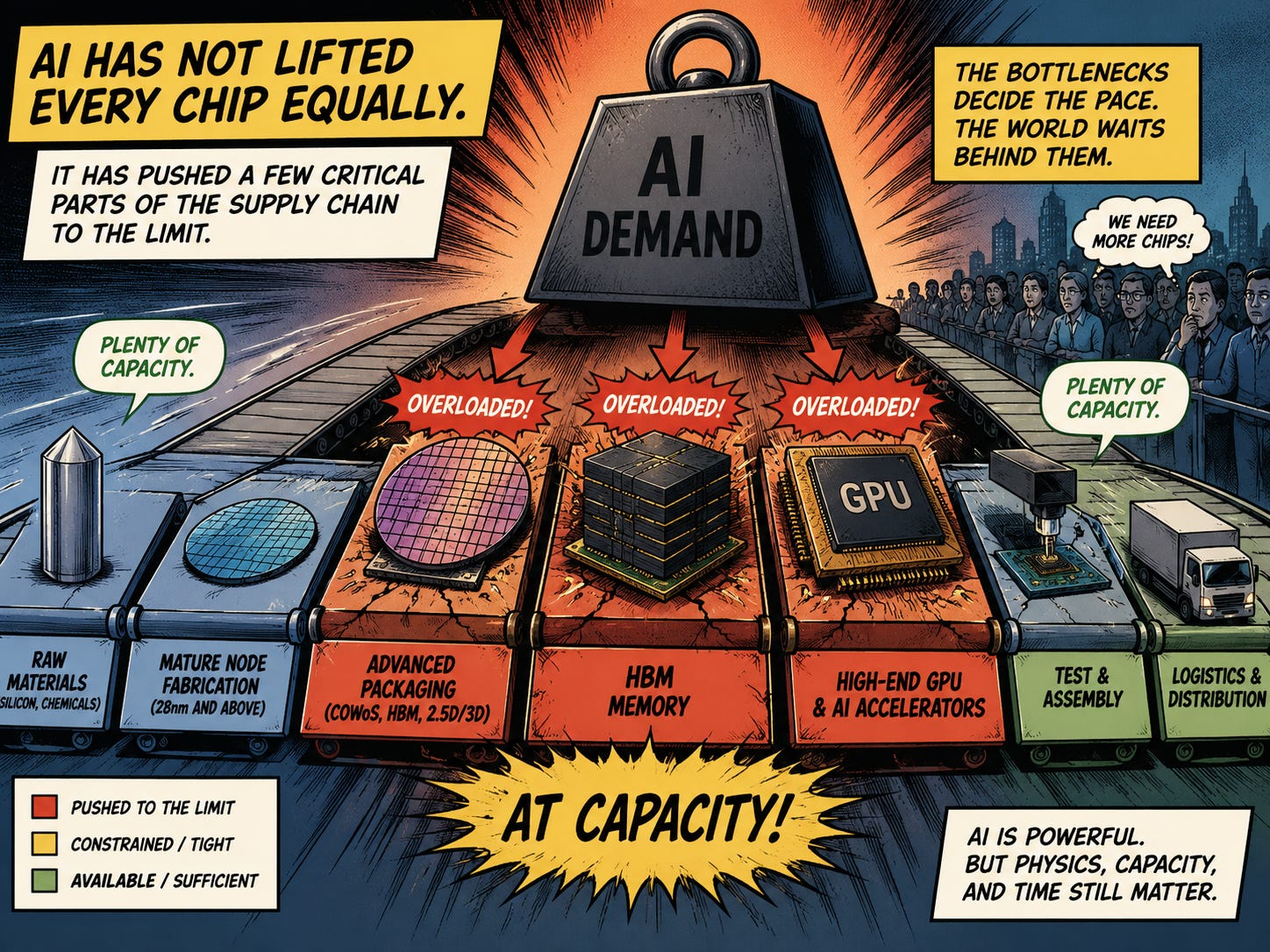

If there is one sentence that captures the semiconductor cycle of 2025 to 2026, it is this: AI has not lifted every chip equally. It has pushed a few critical parts of the supply chain to the limit.

AI has not lifted every chip equally. While the AI boom has created massive demand across the semiconductor industry, the real pressure is concentrated in a few critical parts of the supply chain. High-end GPUs, HBM memory, advanced packaging, substrates, power delivery, and thermal solutions are now being pushed close to their limits. These are no longer ordinary components; they are strategic bottlenecks that determine how fast AI infrastructure can scale. At the same time, many traditional chip segments still have sufficient capacity or even face slower demand recovery.

This uneven cycle shows an important reality: AI is not simply expanding the entire semiconductor market in one smooth wave. It is selectively compressing the most advanced, capital-intensive, and technically difficult layers of the ecosystem. In the AI era, the winners are not just the companies making chips, but the suppliers controlling the bottlenecks.

That is why South Korea’s late-June announcement of a KRW800 trillion semiconductor investment plan matters far beyond a standard capacity-expansion story. On the surface, Samsung Electronics and SK hynix are adding new fabs in the country’s southwest. At the industry-chain level, however, the move is a direct answer to a much larger question: as AI infrastructure becomes the center of global capital spending, who can provide enough memory, packaging, and system-integration capacity with real reliability?

This is not normal capex. It is a national reassembly of the memory stack.

For years, semiconductor investment was framed mainly as a leading-edge logic race focused on 2nm, 3nm, and foundry leadership.

By 2026, the bottleneck has clearly widened into memory and packaging.

AI servers are consuming HBM, DDR5, advanced substrates, high-speed interconnects, and packaging capacity at a pace that is changing the industry’s profit pool. Industry market shows that 3Q26 DRAM pricing even with softer consumer demand. That tells us the price-setting force is no longer PCs or smartphones. It is AI infrastructure deployment. SEMI reinforces the same message: global 300mm memory equipment investment is projected to reach $52 billion in 2026 and $57 billion in 2027. This is not restocking. It is the industry admitting, through capital allocation, that AI memory is now a strategic battlefield.

Against that backdrop, South Korea’s plan is not simply about adding wafer starts. It is about turning product leadership in memory into geographic and ecosystem leadership. Samsung and SK hynix each plan two new fabs, while SK hynix separately outlined KRW400 trillion for the southwestern region and KRW100 trillion for the Chungcheong region.

The implication is clear: Korea wants to bind front-end manufacturing, back-end packaging, local suppliers, data centers, and infrastructure into one national AI-industrial narrative.

Why Korea feels it has to move now

The answer is straightforward: AI memory is no longer behaving like a normal cyclical commodity. It is becoming strategic infrastructure.

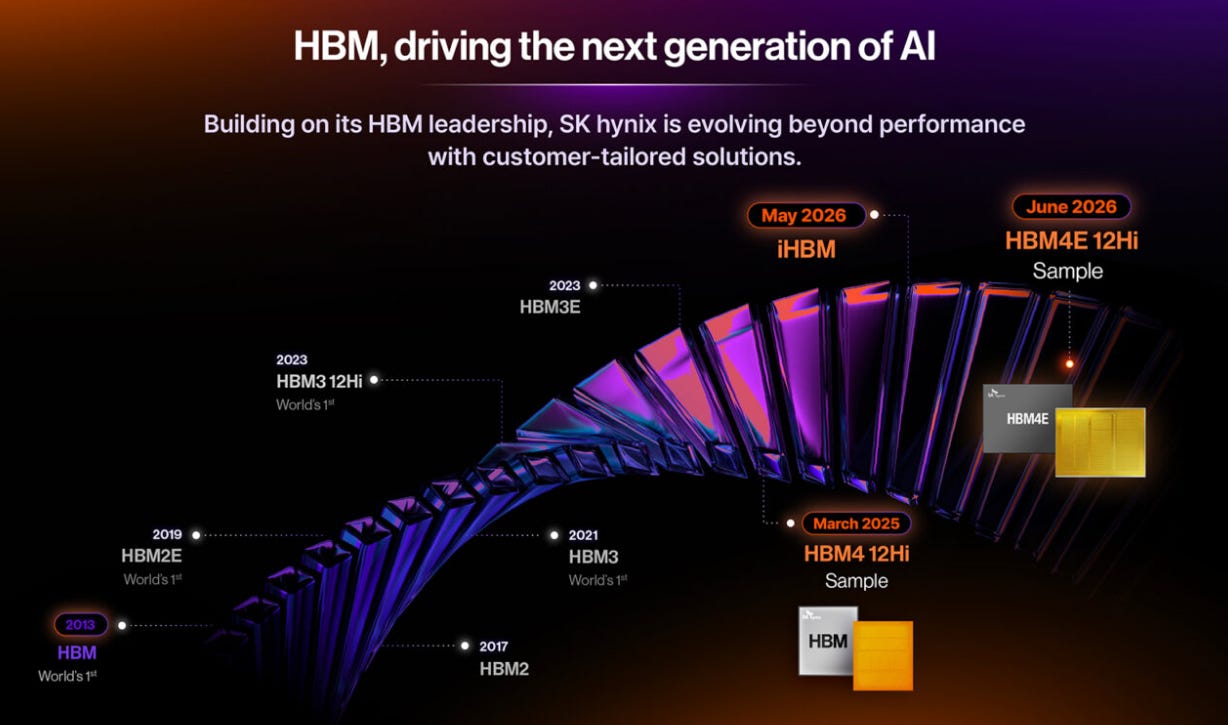

SK hynix has continued to strengthen its position in AI memory. The company announced both the completion of HBM4 development and preparations for its mass production and also showcased its AI memory portfolio centered on HBM3E and HBM4 at major global technology events. HBM4 is a next-generation product designed to address the higher bandwidth and power efficiency requirements of high-performance AI systems.

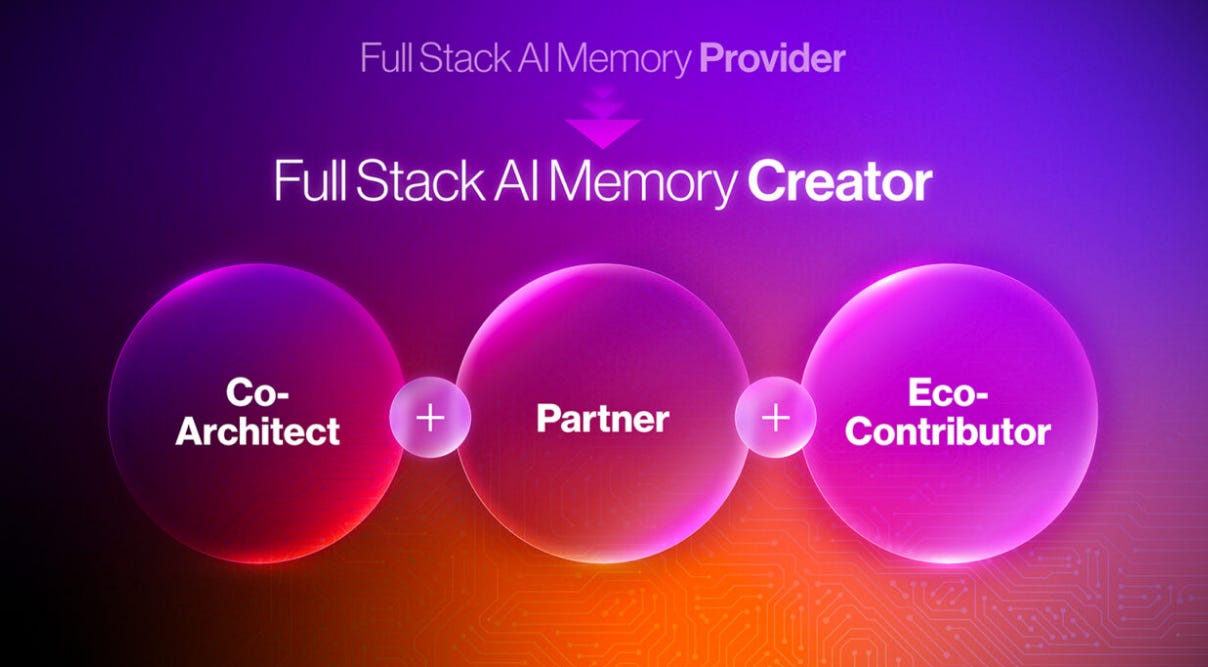

This collaboration model also reflects the vision SK hynix presented at SK AI Summit 2025: becoming a full-stack AI memory creator. At the summit, SK hynix emphasized that its role is evolving beyond being a traditional “provider” that delivers products customers need at the right time. Instead, the company aims to become a “creator” that works closely with customers and ecosystem partners to solve system-level challenges.

SK hynix is also reinforcing its organizational structure and research capabilities to respond more directly to the rapid evolution of the AI ecosystem. Its plan to establish a U.S.-based AI company represents a strategic step toward deeper AI system-level optimization and broader collaboration across the data center value chain. Leveraging its global research network, SK hynix is further expanding its understanding of computing architectures, customer workloads, and next-generation memory solutions designed for future AI systems.

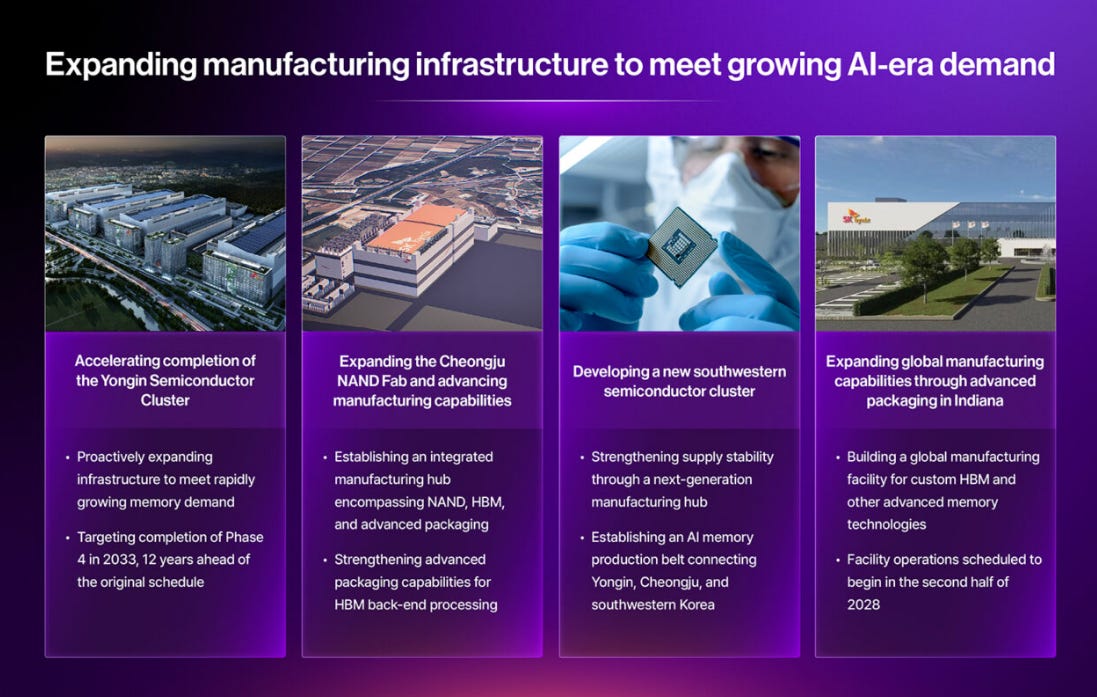

To address the rising demand for high-performance AI memory, including HBM, SK hynix is expanding both its production capacity and advanced packaging infrastructure. Investments in the Yongin Semiconductor Cluster, the Cheongju NAND fab, and southwestern Korea serve as key pillars for reinforcing SK hynix’s domestic manufacturing base. Together with its advanced packaging facility in Indiana, U.S., these investments strengthen the foundation required to enhance AI memory production capability, supply resilience, and customer support.

The Yongin Semiconductor Cluster will serve as a core base for securing long-term memory production capacity. Cheongju M15X is being positioned as a production hub optimized for next-generation DRAM products such as HBM, while Cheongju P&T7 is being developed as an advanced packaging fab dedicated to AI memory, including HBM. The southwestern Korea production belt further extends SK hynix’s domestic manufacturing footprint by linking Yongin and Cheongju into a broader production network. This reinforces the company’s long-term strategy to meet growing global demand for high-performance memory as AI adoption accelerates.

Meanwhile, SK hynix’s advanced packaging facility in Indiana will strengthen its packaging and R&D capabilities for AI memory products and support closer collaboration with North American customers. Together, these domestic and overseas investments show that SK hynix is not only expanding capacity, but also building a more resilient and geographically diversified AI memory supply chain.

Classic memory cycles were defined by sharp price swings, rapid reversals, and broad end-market exposure. The 2026 structure is different because demand is increasingly concentrated in a smaller set of hyperscalers, AI model developers, and large data-center operators. These buyers are deploying longer planning cycles, larger balance sheets, and more aggressive supply commitments.

That shift creates three important consequences.

First, memory capacity expansion is no longer determined only by tool deliveries. It also depends on packaging capacity, power availability, water access, labor, and regional execution. This is why SK Group Chairman highlighted the need for land, electricity, water, and skilled workers. In the AI era, those are no longer secondary constraints. They are core production variables.

Second, announced investment does not mean near-term relief. Markets often treat large capex headlines as a signal that supply will soon normalize. In reality, the path from announcement to environmental review, site preparation, utility build-out, tool move-in, and volume production takes years. In that sense, KRW800 trillion is bullish for long-term supply growth but also a reminder that the near- and mid-term tightness is real.

Third, supply-chain power shifts toward whoever can solve multiple bottlenecks at once. That is why recent weeks have brought not only memory price discussions but also advanced packaging price hikes, mature-node pressure, and policy debates focused on accelerating capacity rather than suppressing pricing.

How the supply chain gets rewritten

This investment wave has at least five major implications.

The first is for memory equipment vendors. Etch, deposition, metrology, cleaning, and process-control suppliers should see better medium-term visibility. But revenue timing will still track actual fab schedules and installation progress, not headline pledges alone.

The second is for packaging and substrate players. Korea’s decision to position Chungcheong as a packaging base is a direct acknowledgment that AI memory competitiveness is no longer about shipping bits alone. It is about integration with GPUs, custom ASICs, interconnect, thermal management, and package-level yield. That keeps OSATs, advanced substrates, test houses, and related backend specialists in the center of the story.

The third is for materials and utilities, which are becoming hidden forms of capacity. Photoresists, specialty chemicals, gases, ultrapure water, transformers, and renewable-energy access are no longer background inputs. They are gating factors for whether announced projects turn into actual output.

The fourth is regional rebalancing inside Korea. The established Gyeonggi ecosystem will likely remain superior in engineering density and supplier clustering. For the southwest and Chungcheong regions to catch up, Korea will need policy incentives, labor mobility, and supplier co-location. In other words, the next stage of Korea’s semiconductor competition is not only global. It is internal and geographic.

The fifth is repositioning pressure on Taiwan, Japan, and the United States. If Korea succeeds in domesticating a larger share of memory manufacturing and packaging, overseas equipment and material suppliers may gain incremental demand, but competing ecosystems will also sharpen their own roles: Taiwan in advanced packaging and panel-level packaging, Japan in materials purity and reliability, and the U.S. in AI system customers, financing, and policy leverage.

The real issue is not willingness to invest. It is execution.

This is the most important point.

The easiest analytical mistake is to translate “investment announcement” into “supply relief is coming.” From an industrial-engineering perspective, the opposite can be true. The larger the project, the more clearly it exposes the weakest links.

South Korea’s decision to push this hub into the southwest has strong political and regional-development logic. But it also raises execution complexity. Can the new region build enough supplier density, equipment service capacity, logistics, housing, workforce training, and partner infrastructure fast enough? That question will determine whether this becomes a true memory corridor or a slower-moving capital promise.

That is also why SEMI’s July 1 letter to the U.S. government is so revealing. The industry is increasingly arguing not for direct market intervention, but for policies that speed up supply formation: consumer tax relief, investment support for equipment and materials, and faster permitting. The underlying principle is the same everywhere: when AI turns certain chips into strategic resources, the scarcest asset is not only fab capacity itself, but the speed at which that capacity can be brought online.

What to expect over the next 12 to 18 months

South Korea’s Survival Gamble: When a Young Generation Stops Believing in Hard Work and Goes All In

SemiVision sees four trends worth watching.

First, capital allocation will keep tilting further toward HBM and AI-linked memory rather than broad-based commodity memory expansion.

Second, packaging will become a key determinant of memory ROI. If CoWoS, FoCoS, CoPoS, and FOPLP remain tight, front-end wafer additions alone will not fully translate into faster system shipments.

Third, pressure between AI-related demand and mature-node supply will widen. Industry media has already warned that AI-related wafer allocation is crowding mature nodes, which means MCUs, power devices, connectivity chips, and other legacy-node components may remain structurally tighter than many buyers expect.

Fourth, policy will act more as a supply-chain accelerator than a price manager. Korea’s industrial clustering strategy and U.S. industry lobbying point in the same direction: governments are being asked to reduce friction, shorten timelines, and improve capex certainty.

To judge whether this KRW800 trillion corridor will materially alter global supply, SemiVision would watch:

whether the southwest and Chungcheong regions publish concrete milestones for land, power, water, and utility infrastructure

whether Samsung and SK hynix provide clearer fab start, tool move-in, and production timelines

whether Korean local suppliers in materials, equipment components, and packaging announce matching expansions

whether long-term contracts in HBM, DDR5, and advanced packaging continue to spread

whether prices and lead times for CoWoS, FoCoS, CoPoS, and FOPLP stay elevated

whether mature-node pricing pressure really extends into 2027, as industry report expects

The significance of South Korea’s KRW800 trillion investment is not just that it is enormous. It is that it reveals a deeper reality:

In the AI era, semiconductor competition is no longer mainly about one node or one company. It is about the execution power of entire supply chains and industrial systems.

In the short term, this plan will not suddenly end AI-related shortages. If anything, it underscores how scarce true execution capacity remains. Over the medium term, if Korea can make this corridor real, it will not only reinforce its leadership in memory. It will also push more bargaining power in the AI supply chain toward memory, packaging, and backend integration.

The key question from here is no longer just who has the most advanced process. It is who can turn the full AI capacity stack into real output fastest.